VAT on medical services and healthcare

VAT where medical professionals are involved may seem a straight forward area of this complicated tax – but is it as straight forward as it seems? The provision of medical care to individuals is exempt for VAT purposes, but does this cover the provision of services of a locum GP, or other doctors supplied through an agency? The key question is who is the locum GP or other doctor supplying their services to?

Is VAT Chargeable?

There are 3 mains areas where the VAT treatment potentially can be wrong, where the supplies may have been treated as exempt, instead of a standard rated VAT that should have been charged.

1. Supplying services to a GP Practice, hospital etc. as a Locum

The first area where common mistakes are made is where a medical professional supplies their services as a Locum to hospitals or other GP practices. The key question is what are the supplies that are being made?

If a medical professional is supplying services to a hospital as a GP Locum, normally their supply is made to the hospital or the GP practice (they will invoice the hospital/GP practice and not the patient direct), and it is that entity that will then provide the medical care. The supply, therefore, is one of staff, which is standard rated for VAT purposes. The diagram below shows how this works.

The contractual relationship is between the medical professional and the hospitals or GP’s practice, and not with the patient, and if anything was to go wrong, it would be the hospital that would be bearing the risk.

However, if the medical professional is billing the patient direct, then this would be an exempt supply, as the medical professional will then be supplying medical care services direct to the patient, and possibly paying a commission then to the Hospital/GP Practice (obviously this would only apply to private practice) as follows:

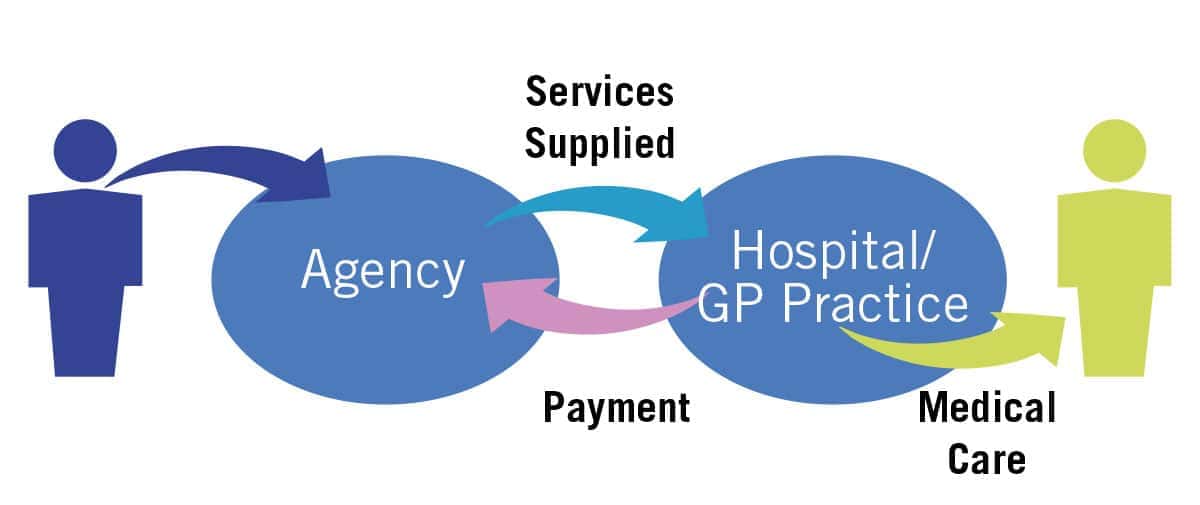

2. Supplying services as an agency

When an agency supplies medical professionals (other than staff subject to the nursing agencies’ concession) in it’s own name to a hospital or GP practice, where the medical professional is working under the control and guidance of the hospital or GP practice, it is making a taxable supply of staff to that entity – not an exempt supply of healthcare. It is the hospital or GP practice which is responsible for providing healthcare to the final patient, rather than the business supplying the staff which has no such responsibility (see the diagram below).

Again, the contractual relationship is between the agency and the hospital, and it is the hospital who bears the risk if anything should go wrong. A taxable supply of staff is made even where the agency is responsible for ensuring that the workers it provides are properly trained and qualified when they work under the control of the third party.

However, if the agency maintains the direction and control of its medical professionals to make a supply of medical care directly to a final consumer, then the agency is providing medical services rather than merely a supply of staff. In these circumstances, the business is making an exempt supply of health services.

3. Supplying medical care direct to patients

For the sake of completeness, the provision of medical care direct to patients without any agency involvement, then this should be an exempt supply of medical care.

What are the implications of VAT being chargeable?

Firstly, the agency or the medical professional may have to register for VAT, depending on their turnover. If the turnover on supplies to hospitals/GP practices where the hospital or GP practice is responsible for the provision of care exceeds £81,000 in the previous 12 months, then you will need to register for VAT. VAT registration is also voluntary, and this is an option to think about to be able to recover some of the VAT you incur.

There is potential that the treatment has been wrong for a number if years, and in which case, there may be penalties and interest chargeable for late registration.

Secondly, once and if registered and as mentioned above, you will be able to reclaim some of the VAT incurred. As you will more than like to be making taxable and exempt supplies, only a proportion of the VAT can be reclaimed, and this requires a calculation to be completed each VAT period.

Need to know more? Fill out the form and we will be in touch or contact Jason Croke directly

Contact Us

"*" indicates required fields

Sign up to our newsletter

Join our mailing list to receive regular updates on

the news and events you need to know about.