SDLT – Non-resident Surcharge

Stamp Duty Land Tax, non-resident surcharge in effect from 1st April 2021

There is a new, additional SDLT non-resident surcharge (NRS), applicable to non-resident persons (or non-resident entities) who acquire property in England and Northern Ireland from 1 April 2021. This new surcharge does not apply to Scotland and Wales, who have devolved powers, but it is likely that both Wales and Scotland will introduce similar measures in due course.

The non-resident surcharge is applicable on the purchase of dwellings. The surcharge will be 2% in addition to the existing SDLT rates. For clarity, that means the normal SDLT bandings, plus the existing 3% surcharge for additional dwellings, plus 2% if the purchaser is non-resident.

If the value of the property is less than £40,000 then the surcharge will not apply, nor will it apply for leases of less than 21 years.

Individuals/ Couples

The non-resident surcharge will apply when one or more purchasers have been in the UK for less than 183 days during any 12-month period PRIOR to the purchase. The technical wording refers to the “relevant period” which is defined as 364 days before the date of the transaction and ends 365 days after that date. “Days” are defined as per the normal residency rules.

The main point to note is that the definition used for “non-resident” is different than the usual residency test for individuals. It is therefore possible that an individual that meets the normal UK residency test for tax, will not automatically meet the residency test for the non-resident surcharge.

The non-resident surcharge can be refunded where the purchaser becomes UK resident. The refund period starts from 364 days before the date of transaction (purchase) and ends 365 days after the date of transaction. The existing 3% additional dwelling surcharge is not refundable unless the conditions for refunding that surcharge are met.

In effect, this captures those who are looking to move to the UK and have acquired property in the last year but have not yet moved, as well as capturing those who are yet to buy a UK property but intend to do so before moving to the UK after purchasing the dwelling.

There is an exception for couples (either married or civil) who are living together at the time the dwelling is purchased, if one of the couple is UK resident (using the SDLT definition) and the other non-resident, then the non-resident can be treated as resident for the purpose of the SDLT non-resident surcharge.

Corporate

For corporate purchases, the usual residency test for corporate entities remains, so a non-UK entity would trigger the charge as would a UK entity that meets the non-UK control test. For example, a UK entity purchasing a dwelling over £500,000 could see the 15% SDLT rate apply, but a non-resident purchasing the same property would pay 17% SDLT. The usual exceptions to this rule apply, such as dwellings held as a property rental business, property developers, etc.

In terms of Trusts, the normal residency rules remain, in terms of Bare Trusts it is likely that where the beneficial owner fails the SDLT residency test, then the non-resident surcharge would apply and very quickly this can become quite a complex area with trust law and tax law inter-twining.

HMRC have not published, as yet, detailed guidance although the draft legislation has been produced and is what this article is based upon. As soon as HMRC release further details then we will update this article with any new or relevant points.

Summary

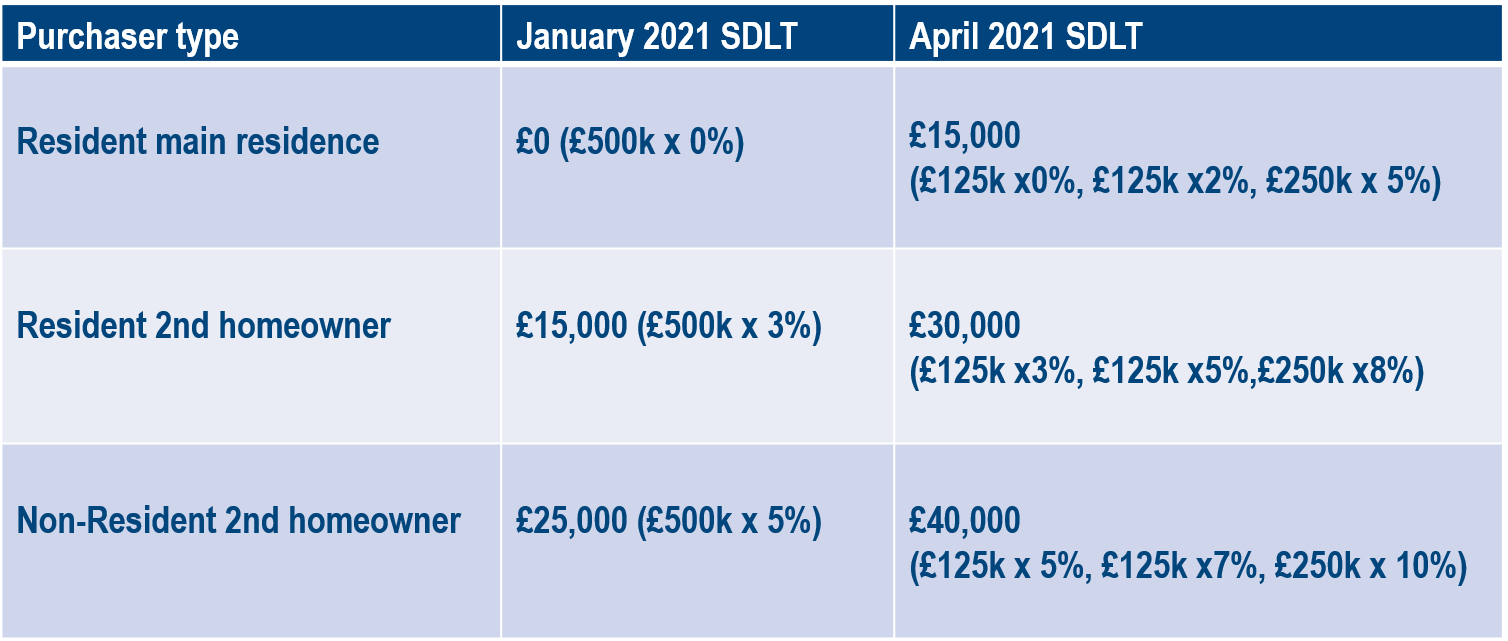

Due to Covid19, the SDLT rates in England and Northern Ireland are temporarily reduced, thus SDLT at Nil rate band is applicable on purchases up to the first £500,000 (from 01st April 2021 this will revert to the first £125,000 being Nil rate, the next £125,000 at 2% and the next £675,000 at 5%).

The above rates are the base rates, excluding the 3% surcharge and the non-resident surcharge. But there are still opportunities here to save SDLT by purchasing before the end of March 2021 whether you are UK resident or non-resident.

For example, take the purchase of a dwelling in England, costing £500,000 and the purchase takes place either in January 2021 or in April 2021:

The above are just examples of the impact of the temporary reduced SDLT rates and the application of the non-resident surcharge. The above is very simplistic and does not factor in various exemptions or alternatives such as Multiple Dwelling Relief, so the examples above are not definitive in their calculation.

Please get in touch if you would like further information or advice

Contact Us

"*" indicates required fields

Sign up to our newsletter

Join our mailing list to receive regular updates on

the news and events you need to know about.