Domestic Reverse Charge for Construction Services

What is Domestic Reverse Charge for Construction Services?

The mechanism is an anti-fraud measure, which is prevalent in the construction sector and these rules are therefore required to reduce the VAT losses that HMRC incurs. In essence, as the sale is no longer subject to VAT by the seller, the opportunity for VAT fraud is reduced considerably.

If supplying services that meet the conditions, then you do not charge VAT and the customer accounts for VAT under reverse charge.

Before looking at the conditions in more detail, the first point to note is that the scheme does not apply when the supplies you are making or receiving are zero rated – so services related to the construction of a new dwelling(s) is zero rated and so reverse charge is not relevant.

The reverse charge does not apply to supplies of materials only (i.e. builders’ merchants) but reverse charge will apply where you supply both materials and construction services and if there is a mixture of goods and services, the whole supply counts as a single supply of services and subject to reverse charge.

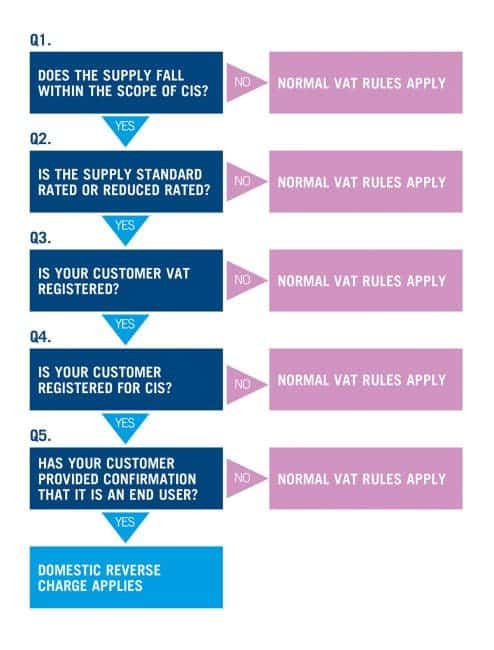

HMRC have produced a flowchart (see below) which should be used for each transaction, but some words require a definition/clarification: –

End User

End users are consumers (B2C) or final customer/end customer (B2B). A consumer is therefore an individual (man on the street) and a final customer is the final person in the chain for whom will own the property.

Domestic Dwellings

A new house building project will likely be zero due to construction of a new dwelling being zero rated and, in that regard, would not be subject to reverse charge, it would just be zero rated naturally.

If involved with refurbishment or extension works to existing dwellings, then that work would usually be standard rated, and you would need to identify the end user to determine VAT treatment. In most cases, the end user will be the homeowner (B2C) and so not under this scheme. However, if you are a sub-contractor to a main contractor, your supply to the main contractor would be reverse charged and the main contractors supply to the final customer, standard rated.

Commercial Property

Generally, if a main contractor identifies the status of its sub-contractor as falling under CIS, then the sub-contractor will use the reverse charge and the main contractor will account for VAT to HMRC.

A supplier will not automatically know if their customer is an end user or not. The default position is that if all the other conditions are met (customer and supplier is CIS registered, customer is VAT registered, supply would ordinarily be standard or reduced rated), then the supply falls under the reverse charge until such time the customer produces evidence, they are an end user.

Consequences of these new rules

Cashflow is the main impact. Main contractors will have an improved cashflow as they will not be paying out VAT to sub-contractors and the main contractor processes the supplier’s invoices via reverse charge, declaring and reclaiming VAT on the main contractor’s VAT return.

Sub-contractors will see poorer cashflow, as sub-contractors will no longer have the benefit of holding onto VAT until it is due to be paid to HMRC.

Sub-contractors could move to monthly VAT returns on the basis they will most likely be in a repayment (refund) position, this is because they will still incur input tax on materials and overheads which may well be greater than the output tax due and especially so if there is Nil output tax due because all sales are reverse charged.

If you can’t switch to monthly accounting then the business will still likely be in a repayment (refund) position but will have to wait 3 months to get it from HMRC, therefore a cashflow buffer may be required to cover the period between VAT returns.

Administrative Changes

In terms of practical administration, the business will need to clearly identify supplies that are normal/VATable and supplies which fall under reverse charge. Cloud accounting software should already have the facility to code reverse charge transactions. It may be identified as “DRC” (Domestic Reverse Charge), both Xero and QuickBooks have already implemented.

For the invoice, it would only show the net value and some wording to the effect of “this invoice is subject to domestic reverse charge, customer to account for VAT at 20%”. It is a requirement that the invoice identifies what the VAT rate is (20% or 5%) so that the customer knows what rate to apply, but we cannot show the VAT in the numeric part of the invoice else they may think the invoice has VAT charged on it and not do the reverse charge at their end.

If you operate under self-billing with your sub-contractors, then their invoice, which you raise for them, would state.

For a sale you make under reverse charge, Box 6 shows the net (sales excluding VAT) and Nil in box 1 (output tax due).

For a purchase you make under reverse charge (sub-contractor billing you), you would record in Box 7 (purchases excluding VAT) the net value on sub-contractors’ invoice.

You would then perform a reverse charge movement which would see you calculate 20% (or 5%) of the sub-contractor’s invoice and declare output tax in Box 1 and then reclaim same value as input in Box 4.

Use this flowchart to help.

If you would like any further guidance please fil out the form below or contact Jason Croke our VAT Director who will be happy to help.

Contact Us

"*" indicates required fields

Sign up to our newsletter

Join our mailing list to receive regular updates on

the news and events you need to know about.